April 2026

The Iran Conflict and Its Impact on Markets

Seven weeks into the US-Israel war with Iran, the market and economic consequences are becoming clearer. Brent crude oil prices are up roughly 50% and remain highly volatile, whilst equity markets are changing daily, rising and falling quickly as the conflict unfolds. Volatility has increased across all asset markets.

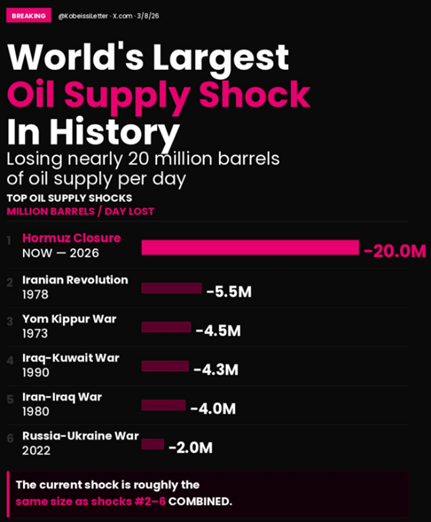

For investors, the centre of gravity remains the Strait of Hormuz, through which a significant share of global oil and liquefied natural gas (LNG) transits each day. With shipping traffic through the Strait falling sharply and continuing to face disruption, the question is no longer whether there is a supply shock, but how deep and how prolonged it will be. This note sets out where we see the impact landing, and what it means for portfolios.

The supply shock

The initial physical shortfall in oil supply was cushioned by three factors: strategic reserve releases from the International Energy Agency, the re-routing of Saudi oil supply through the Red Sea, and the continuation of China-linked flows through the Strait. As those reserve releases are exhausted, the supply shock is moving closer to the 20per cent reduction in global oil supply that was long quoted by market commentators. The impacts and shortages are likely to intensify, with Asia feeling the impact first given its dependence on Gulf oil and gas.

Impacts beyond oil

Oil and natural gas are feedstocks for more than 95 per cent of manufactured goods, so the shock extends well beyond energy prices. Methanol prices -supported by the Gulf, which supplies around 40 per cent of global output – have already risen 50 per cent. The region also accounts for 43 per cent of global urea (nitrogen fertiliser) production and 44 per cent of global sulphur, both critical fertiliser inputs. This creates a second-order risk to food prices.

Farmers making planting decisions now may respond to higher costs and reduced supplies availability by planting less. Greater uncertainty around yields is therefore likely to translate into higher fresh food prices over time. Helium, a by-product of natural gas processing used in semiconductors and medical imaging, has doubled in price following disruptions to Qatari supply. LNG prices have also increased.

Economic and inflation implications

We expect the economic impact to diverge meaningfully across regions. Inflation expectations in the United States have so far remained relatively stable, reflecting US self-sufficiency in oil production and refining. However, elsewhere inflation expectations have risen since the start of the conflict, including in Australia. If the disruption persists, we expect US inflation expectations to move higher as the broader, non-energy effects of the shock feed through.

Before the conflict, markets had been expecting most central banks would cut rates this year, except for Australia and Japan. The inflation impulse complicates this path. While markets have already trimmed rate-cut expectations, the response has been relatively muted as investors await clarity on duration and severity of the supply shock.

Implications for Australia

Australia is a very wealthy country, especially within the Asia Pacific Region, and is therefore in the fortunate position of being able to import fuel at much higher prices, outbidding countries who could not pay the higher spot price. However, low domestic reserves and limited refining capacity mean we are reliant on imports at higher prices.

Some Australian businesses have already introduced fuel surcharges, adding to inflation pressures. The halving of the fuel excise supports household wallets in the short term, but by keeping demand elevated it also reduces the natural demand destruction that higher prices would otherwise create. Once the conflict eases, we would expect Australia to rebuild fuel reserves back toward mandated levels, which should keep domestic prices elevated even after shipping through the Strait normalises.

Market outlook

No one can predict the outcome of the conflict in the short term or the path forward. We can say with more certainty however that the outcome of the conflict is inflationary, and this inflation impulse will persist for some time beyond any re-opening of the Strait.

There are several constraints pointing to a resolution sooner rather than later. The fiscal cost of the conflict to the US is meaningful given an already stretched position, US midterm elections may provide a political off-ramp, and domestic support for the conflict is limited. That said, history cautions against assuming a quick reversal, and markets are not yet fully pricing a prolonged scenario. The complexity of negotiations increases the risk of an extended period of intermittent closures of the Strait, an outcome that would be particularly disruptive for the global economy.

Portfolio implications

Our base case is that inflation remains stickier, limiting central bank’s ability to lower rates and raising the possibility of further tightening in some economies. Periods like this reinforce the value of genuine diversification across asset classes, sectors and currencies, rather than reactive repositioning on headline risks.

We are not making short-term or reactive portfolio changes in this environment, as there is no reliable way of making an informed decision on near-term events. Instead, we continue to rely on our long-term approach to investment selection and portfolio construction and will make changes accordingly as the medium to long-term outlooks for investments evolve.

We are closely monitoring energy-intensive sectors, inflation-sensitive assets, and interest rate exposed positions, and will adjust where the evidence supports it.

If anything in this note raises questions specific to your circumstances, please get in touch.

Written by Christopher Lioutas

Chairman – Harbourside Investment Management