April 2026

As the daily news flow of actions in and around Iran continue, below is a brief update on events

and Genium’s views on market movements and expectations.

Conflict update

- Oil prices are now up ~50% since the beginning of the conflict 4 weeks ago.

- Markets have broadly sold off in tandem so far, while volatility has risen across both equities and bonds.

- Many high-ranking leaders in Iran have been killed, with the head of their Navy the most recent confirmed senior casualty.

- It appears that Israel and the US underestimated how resilient Iran would be in continuing the fight beyond the first few days.

- Media rhetoric of Iran and US negotiations are unclear; however, it is reasonable to expect that conversations are occurring. We do not feel these reports give any insight into the duration of the conflict.

- As noted below in detail, the longer the conflict goes, the clearer and more significant the economic impact will become. This is true even if the conflict was to end in the next two months, due to the flow on impacts of a large physical supply shortage.

Energy Shock

- Oil supply shock so far has been about 5% of global supply, dampened by:

- International Energy Agency (IEA) reserve releases

- Re-routing of Saudi oil through the Red Sea terminal

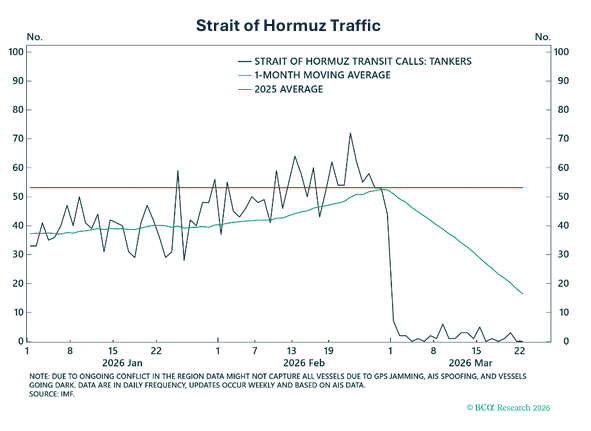

- China-linked supply passing through the strait (as the chart below shows, this is still a very small volume relative to normalised levels)

- Markets did not respond to the IEA reserve release.

- Now that the IEA has released much of their reserves, physical oil supply shock goes from 5% to 10%. The 20% supply shock noted by most observers would be worst case scenario.

- If the strait remains effectively closed for another 2 weeks, physical shortages will intensify.

- This will have a larger economic impact on global economic activity and global trade, starting in Asia first due to the region’s reliance on gulf oil and gas.

- Many countries will look to start building up their reserves, which is challenging for countries without refining capacity (Australia) and will stoke inflation.

- Gulf LNG exports only represent 3% of natural gas consumption, however gas prices are set at the margin hence the price jumps.

- Coal price impact is expected to be much lower than 2022 Russian coal export ban, however, have still ticked up due to fuel switching in Asia.

Impacts beyond oil

- Petrochemicals made from oil & natural gas provide the building blocks for over 95% of all manufactured goods including plastics, fertilizers, pharmaceuticals and synthetic fibres, and are critical inputs in construction, automotive and healthcare industries.

- One example is methanol; 40% of the world’s methanol supply comes from the Gulf Region and is now stranded. Methanol prices have risen 50%.

- The Gulf region is also a major hub for agricultural exports: in 2024, it accounted for 43% of global urea, 44% of global sulphur and 27% of global ammonia supply. Urea and ammonia are critical components of nitrogen fertilizers and sulfuric acid is an essential input for producing phosphate fertilizers.

- Farmers making decisions about planting volumes today would be cognisant of the risk of fertilizer supply disruptions, which would reduce food supply over subsequent years, therefore increasing inflation.

- Helium is a byproduct of natural gas processing and is used in semiconductors and medical imaging. Qatar accounts for 34% of global supply; spot prices have risen by 100% since the war began.

Economic Impact

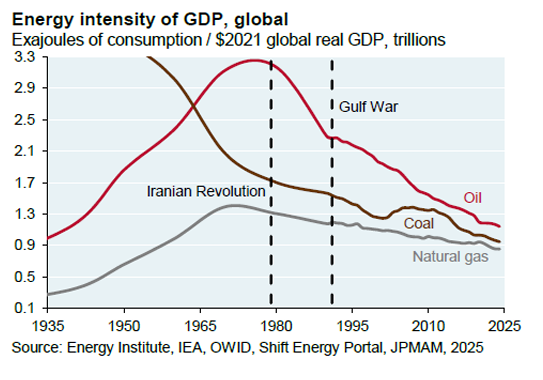

- Positively, the oil intensity of GDP has halved since 1990 Gulf war, after a peak in Positively, the oil intensity of GDP has halved since 1990 Gulf war, after a peak in 1970. This will dampen the impact of a persistent oil supply shock.

- Natural gas intensity has also steadily dropped despite natural gas consumption doubling since the intensity peak.

- Substantial improvements in efficiency have driven this outcome.

- There is a limit to energy efficiency benefits in the event of a large supply shock.

- Most of the impacts noted above are inflationary if the conflict persists, however this will be dampened by any subsequent demand destruction.

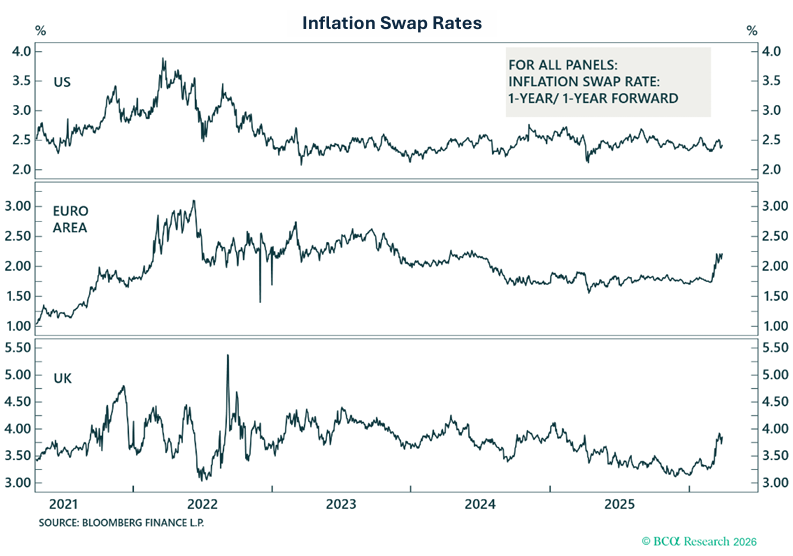

- We expect that if the conflict persists, the impact across economies will diverge. This is seen most clearly in the chart below on inflation swap rates (a proxy for 1 year inflation expectations), where US rates have hardly moved compared to UK and Euro rates.

- This is likely due to the US being self-sufficient with their own oil and refining capacity.

- If the conflict persists, the US will likely see inflation rise too, which is currently not being priced by markets.

Market Impact

- According to JP Morgan Equity Strategy & Quantitative Research, if $120 oil were sustained for 6 months, annual S&P 500 EPS estimates would decline by $12.70 or 4% of consensus EPS of $317 per share.

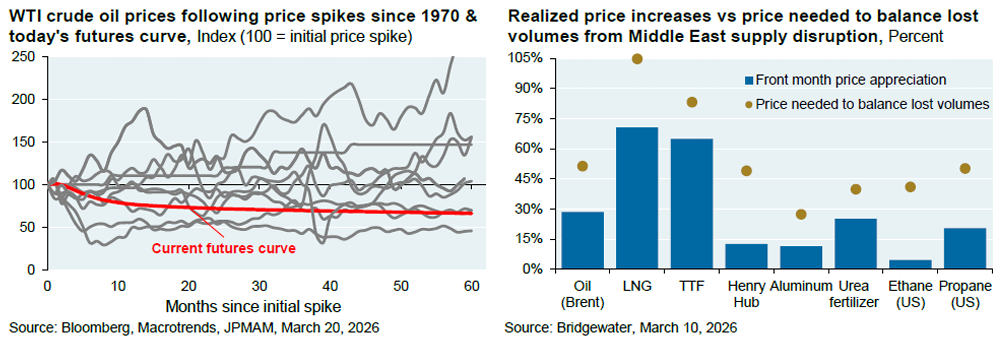

- 100% price spikes to the oil price normally coincide with equity market declines, however we are not at the level of price spike yet.

- Only 4 out of 10 oil supply shocks since 1970 have resulted in quick reversals to lower prices.

- If the supply constraint is not resolved quickly, prices across almost all commodities will need to remain elevated to adequately destroy demand or elicit new supply.

- We also expect the impact across countries to diverge more as the conflict continues.

- Some poorer EM countries (e.g. Cambodia, Sri Lanka) will struggle if they don’t have domestic refining capacity, as they do not have the capital to import enough fuel at the spot price to meet domestic demand.

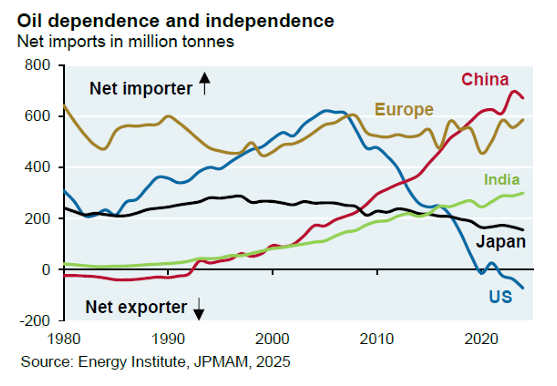

- Among major economies, the US stands out as being a net exporter and not dependent on oil imports for fuel.

Australia

- As a rich country, Australia should be able to continue to import fuel, although we will have to pay high spot prices to get it on shore.

- Consumers are now acutely aware of Australia’s low reserve levels. We are likely to see this built up back to obligated levels once war risk subsides, which will keep prices elevated beyond the end of the conflict.

- Australian businesses have applied levies very quickly in response to higher fuel prices, which is also inflationary.

- Halving the fuel excise tax supports Australian wallets in the short term and will also keep demand at normal to high levels, however this will become hard to manage if supply slows meaningfully as it will reduce the natural demand destruction that higher prices would normally create.

Outlook

- The duration of the conflict will have a major impact on economic outcomes as well as any subsequent portfolio decisions or changes. We are watching for any clear signs of an end to the conflict closely.

- Many of the impacts noted above are inflationary. This will have flow on effects for many central banks around the globe where there have been expectations of rate cuts. Markets have already started to change interest rate expectations, but reactions have been muted so far, pending clarity on the duration of the conflict.

- US Midterm elections present a constraint for the Trump Administration, as the US population is largely unsupportive of the war. This provides increased incentive for Trump to find an off- ramp.

Written by Christopher Lioutas

Chairman – Harbourside Investment Management