March 2026

US/Israel attack on Iran

What has happened?

It’s now been ten days since we awoke to news that Israel and the US had launched large, coordinated air and missile strikes across Iran.

While the lead-up to the strike is now a faded memory for most, it followed months of on-again, off-again, negotiations between the US and Iran over Iran’s denuclearisation. The talks repeatedly stalled around the main issue: the US insisting on a full denuclearisation and Iran’s refusal to accept it.

As negotiations broke down, US and Israeli military forces raised their readiness across the Middle East, triggering volatility in energy markets – particularly oil. Based on news at hand, it appeared the Israeli’s were eager to launch a pre-emptive attack (given critical intel they had obtained) which effectively compelled the US to join their ally in the offensive, a decision later confirmed by the US Secretary of State. The initial wave of strikes targeted Iranian military bases, air-defence systems, command facilities, and government compounds and resulted in the deaths of several Iranian leaders. Iran retaliated by striking Israeli territory and US defence bases through the Middle East, drawing other Middle East countries into the conflict.

Escalation points since the initial attack have seen the closure of the main shipping lane through the Strait of Hormuz, resumed fighting in southern Lebanon between Israel and Hezbollah, continued strikes inside Iran with subsequent retaliation on US bases and US/Israeli military assets across the region. Civilian casualties continue to rise.

Paths from here

Information remains fluid here, and whilst there are many outcomes that could eventuate. However, there are three main paths moving forward:

- Continued conflict followed by negotiated de-escalation – the Trump administration has mentioned a 5–7-week campaign

- Regional war across multiple fronts – with severe regional instability and large economic disruption

- Iran regime de-stabilisation – internal power struggles, collapse of Iranian proxy network, realignment of regional power balances

The market will continue to price each of these outcomes on a daily basis.

Market reaction

Early on, markets largely exhibited nonchalance to the conflict – the same behavioural traits the market exhibited in the two most recent conflicts. Price action was centred in rising oil prices on supply concerns, whilst commodity prices also saw some positive action. Equity markets saw some weakness but largely around the edges with investors seeking out more defensive names/sectors, government bond yields rose (prices lower) as investors focused on inflationary concerns rather than outright risk, whilst currencies largely reacted as expected with investors seeking out safe havens.

The escalation points for markets largely came in the last few days of trading as investors focused on the repercussions of an extended closure of the Strait of Hormuz whilst concerns grew with the Trump administration’s poor responses regarding plans for a resolution/end to the conflict. Interestingly, the Strait of Hormuz isn’t physically blocked but rather closed for insurance-related and safety reasons.

Regarding the Strait of Hormuz, some key facts to understand:

- Roughly 17-20 million barrels of oil per day transit through it

- That equates to roughly 20-25% of global oil supply

- Roughly 130-140 ships transit through it per day.

Markets are increasingly concerned of an elongated conflict with severe and significant disruptions to global oil supply. Oil prices had risen into the US$60 range leading up to the initial strike, rose above US$70 on the strike, and spiked above US$110 (close to US$120 intra-day). They have since settled below US$90 a barrel at the time of writing.

What we’re watching

Obviously, there’s plenty of moving parts, so much so that even this piece is at risk of being stale as it is being written! Outside of the broadening of the conflict to a more regional setting, and the potential involvement of other actors, we are watching the following more closely:

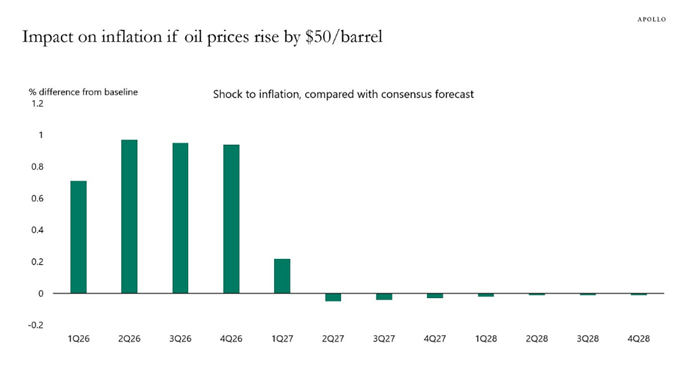

- Inflation – particularly as it pertains to central bank decision making. Direct impacts include fuel and energy prices whilst indirect impacts include shipping, logistics, food production, and manufacturing. Japan, India, and Europe are most exposed here.

- Global growth – higher oil prices reduce real household incomes and increase business costs, whilst broader uncertainty might see consumption and investment curbed. Large oil importing countries (China, India, Germany) are the most effected whilst major oil shocks historically have preceded recessions.

- Stagflation – a prolonged oil shock leading to a mix of higher inflation and lower growth, making central bank decision making (and portfolio construction) extremely difficult.

- Financial markets –

- Equities – negative sentiment could impact broader equity sentiment, but some areas of the market are more exposed than others depending on certain factors. Examples include energy-intensive sectors/companies and consumer discretionary stocks, in addition to companies trading at lofty valuations, whilst the energy sector benefits.

- Bonds – mixed outcomes, which goes someway to explain the mixed reaction from bond markets since the conflict began. For example, the higher inflation impact puts upward pressure on bond yields whilst the negative growth impact puts downward pressure on bond yields.

- Currencies – beneficiaries potentially include oil exporters (Saudi Arabia, US, Russia, UAE) and safe-haven currencies (USD, Yen, Swiss Franc).

What to do?

For now, we think investors should remain relatively calm, but we know that is difficult in the digital / AI age. Portfolios are broadly well positioned to withstand many of the concerns noted above and we stand ready and willing to act depending on how things evolve from here. Our outlook for the year prior to this conflict was less cautious than we were 1-2 years ago, and that undercurrent remains, though is somewhat complicated by the evolving conflict which we continue to watch closely, and hope comes to a swift end.

We’ll keep you informed if anything of significance changes, but in any case, please reach out to your adviser if you have any questions or concerns.

Written by Christopher Lioutas

Chairman – Harbourside Investment Management